AASB S2

Mandatory Climate Reporting

Every element of our program has been deliberately designed to support smooth implementation.

We translate AASB S2 into clear decisions, practical actions, and systems that fit how real businesses already operate.

Directors, project teams, and supporting functions receive tailored briefings aligned to their specific responsibilities, decision rights, and knowledge needs.

The right information, to the right people, at the right time.

Sequenced delivery that matches your capacity and timelines.

Work is spaced, prioritised, and delivered in a logical order so teams can focus on what matters now, without trying to do everything at once.

Implementation guides, checklists and pre-prepared disclosures ready-to-go

We deliver the working materials alongside the advice, so your team has everything needed to progress each stage with confidence.

AASB S2 creates a process for identifying and responding to climate-related risks.

AASB S2 asks companies to do four key things

Understand how climate change may affect your business

Act on the risks and opportunities identified

Explain your approach clearly in an annual report

Ensure what is reported is accurate and put into practice

By including this information in an annual report, it allows investors, lenders and creditors to understand the potential impacts climate change may have on the business’ revenue and expenses, debt, and future planning.

AASB S2 is not about producing a report - it’s about building a climate response your business can stand behind.

Our work is grounded in law, shaped by how businesses actually operate, and focused on reasonable decisions rather than unnecessary complexity.

Do you need to report under AASB S2?

Reporting begins in phases depending on your business size, and is required if you meet two of the three qualifying criteria.

Group 1

Starts FY26

Revenue: $500m+

Consolidated Gross Assets: $1bn+

Employees: 500+

Or 2025 for calendar year reporting

Group 2

Starts FY27

Or 2027 for calendar year reporting

Revenue: $200m+

Consolidated Gross Assets: $500m+

Employees: 250+

Group 3

Starts FY28

Or 2028 for calendar year reporting

Revenue: $50m+

Consolidated Gross Assets: $25m+

Employees: 100+

If you don’t quite meet the thresholds but are close, we recommend starting to prepare well in advance.

Early preparation means the work can be staged over time, rather than rushed under reporting deadlines.

Less time working out what to do.

More time getting it done.

A structured combination of briefings, workshops, guides, and checklists provides a clear pathway from first briefing through to completed reporting.

Workshops across each of the four AASB S2 pillars

We run structured sessions on Governance, Risk & Opportunities, Strategy, and Metrics & Targets to bring relevant teams up to speed on what is required and why, clarifying the core intent of the standard and the actions needed to progress.

Detailed implementation checklist and draft disclosures

We provide your team with the exact materials needed to deliver the required program, including structured checklists, practical templates, and draft disclosures ready to be populated with your specific decisions.

Facilitated climate risk workshop

This is the cornerstone of AASB S2. We get hands-on with your teams to identify, evaluate, and prioritise climate risks, creating a clear foundation for governance, strategy, and reporting.

Director’s Briefing

A targeted board briefing that translates AASB S2 from abstract reporting requirements into clear director duties, highlighting where judgement must be exercised, what must be defensible, and the exposure created when climate disclosures outpace the supporting evidence.

Guided sessions on key decisions

Structured support to help you making key decisions required under the standard, including climate scenarios, risk timelines and severities.

Ongoing implementation support

We stay alongside your team through implementation with regular check-ins, responsive troubleshooting, and practical guidance as new questions, risks, and board decisions emerge.

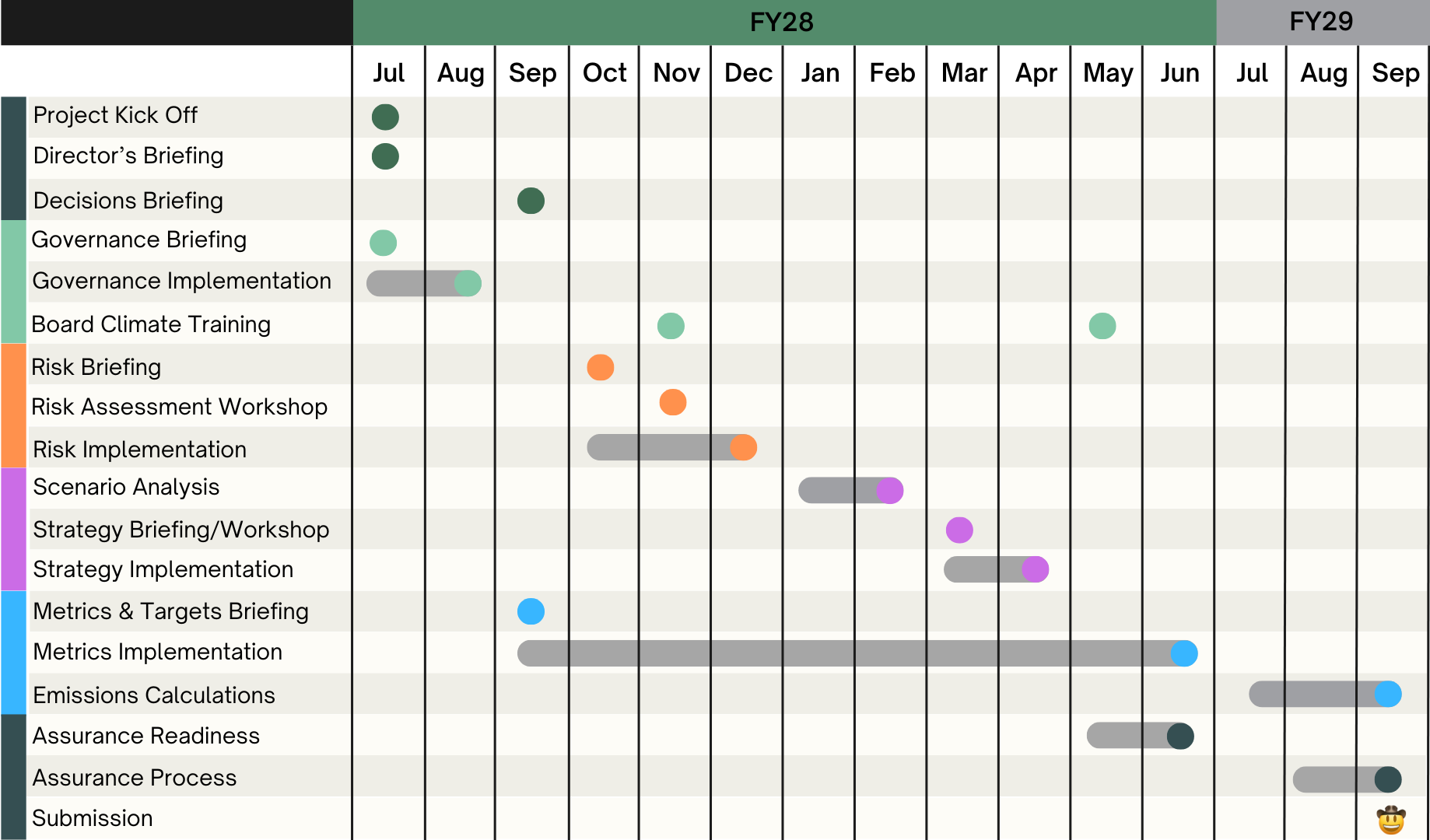

Implementation will take at least a year, and we suggest starting early

Illustrative timeline for a one-year implementation program for a Group 3 business:

Request an initial briefing

Share your contact details and we will provide an overview of what AASB S2 will require for your organisation.